The financial sector is now in a state of transition, initiated by the burgeoning technological advancements that affect consumers’ ways of engaging with their financial information. Open banking, which was initiated in the European Union (EU), is emerging in America and holds potential to change opportunities for customers and companies, including startup financial and traditional banks.

Open banking is the process of sharing customers’ data between banks and other third-party financial service providers. Open banking enables effective transfers of information between the traditional financial organizations and the innovative fintech players using APIs.

The U.S. has not gone as far as adopting regulations as extensive as the EU’s PSD2, but it is gradually nudging into the open banking regime.

What is Open Banking?

Open Banking refers to the proposition whereby third party providers (TPPs) are given permission to access customer’s financial data with the customer’s prior consent. These third parties, who may include credit and financial institutions, financial technologies firms, personal financial applications and other related service providers, use the data to develop products, services and tools.

The first principle of Open banking is to promote competition and innovation in the retail banking market.

The Current State of Open Banking in the U.S.

Open banking in the United States is still a relatively young concept that is just slowly being introduced in a more organic and market-driven approach even though it has become one of the many core elements of the future of financial services.

The U.S. has not, like other jurisdictions, introduced federal laws that compel openness or open banking as seen in the EU or the UK. However, the US has taken a longer process of global, fees-based, and market reforms with drivers and incentives that call for innovations from banks, fintechs, and supervisory agencies.

Open Banking in the United States Today

- The Role of APIs: Many U.S. banks have already started adopting APIs to enable the secure access of customer data which is one of the foundational concepts of Open Banking. Big American banks such as the JPMorgan Chase and Bank of America have incorporated API technology.

- Consumer Demand for Financial Innovation: There is growing demand among consumers in the United States for the development of mass personalization in financial services.

Mint, Robinhood and Venmo are representative of modern applications that have received a lot of attention, which shows that consumers are willing to part with their money information in order to be offered a more personalized service. - Security and Data Protection: Security of the data in the context of the United States’ financial system is an important issue. Therefore, the US banks and the Fintech firms are increasing their level of security features such as encryption, multiple factor authentications and the consent management tools for consumers.

Overview of the Current State of Regulation in the United States of America

Although there is no unifying framework of what could be called Open Banking in the US, as there is in the EU or UK, there are multiple regulations and ongoing initiatives that will naturally create the necessary basis for the implementation of Open Banking principles.

The work being carried out in this regard is evidence that there is a slow but sure understanding of the latter proposition in the financial space and moving to an open, interconnected, and competitive environment that supports consumers, producers, and innovators.

There is appreciable progress being made towards Open Banking within the United States from consumer data right, protection of privacy, and the activities of the various industries.

- Dodd-Frank Act & CFPB: In 2010, the Wall Street reform – known as the Dodd-Frank Act – founded via the Consumer Financial Protection Bureau (CFPB) the Consumer Access to Financial Records rule that provided consumers the rights to access their financial data – an early manifest of Open Banking.

- Data Privacy & Consumer Rights: New legislation including CCPA increases carriers’ and consumers’ control over financial information, thus indirectly promoting Open Banking concepts.

- Industry Standards: Thus, other organizations, such as the Financial Data Exchange (FDX), are fostering API security standards to develop best practices for data sharing in the finance industry.

- OCC’s Role: In this global digital era, the Office of the Comptroller of the Currency (OCC) has initiated federal charters for non-bank financial firms to compete and innovate the Open Banking environment.

Open Banking in the U.S.: Emerging Opportunities & Threats

While the U.S. has no official rules for Open Banking it is an ideal market for development due to consumer desire for innovation and more choice. It presents a more connected environment for providing a range of financial services and products at the consumers’ disposal.

As the Open Banking system advances across the world, it is possible that the American institutions will follow examples and incorporate the standards. Undoubtedly, there are important opportunities, but there are also main risks like data privacy, regulatory apprehension, and integration of different systems to enhance the usability of Artificial Intelligence technology at a large scale.

- Increased Consumption of Online Financial Services

The use of such services as digital wallets and robo-advisors becomes more widespread daily, and that is why people need an open financial environment. Open Banking supplies a unified architecture to meet this demand. - Increased Competition

Open access and its sharing of data owned by the customer with third parties help to create competition between the traditional banks and the new Fintechs, thus bring out efficiency and productivity for both sides. - International Cooperation

Due to the international Open Banking standards, there is a high possibility that the US institutions may implement the same hence expanding the market’s growth and encourage collaboration. - New Financial Products

Open Banking can work to develop new product solutions for customers, such as custom savings, investment products and services, as well as sophisticated budgeting. - Challenges to Overcome

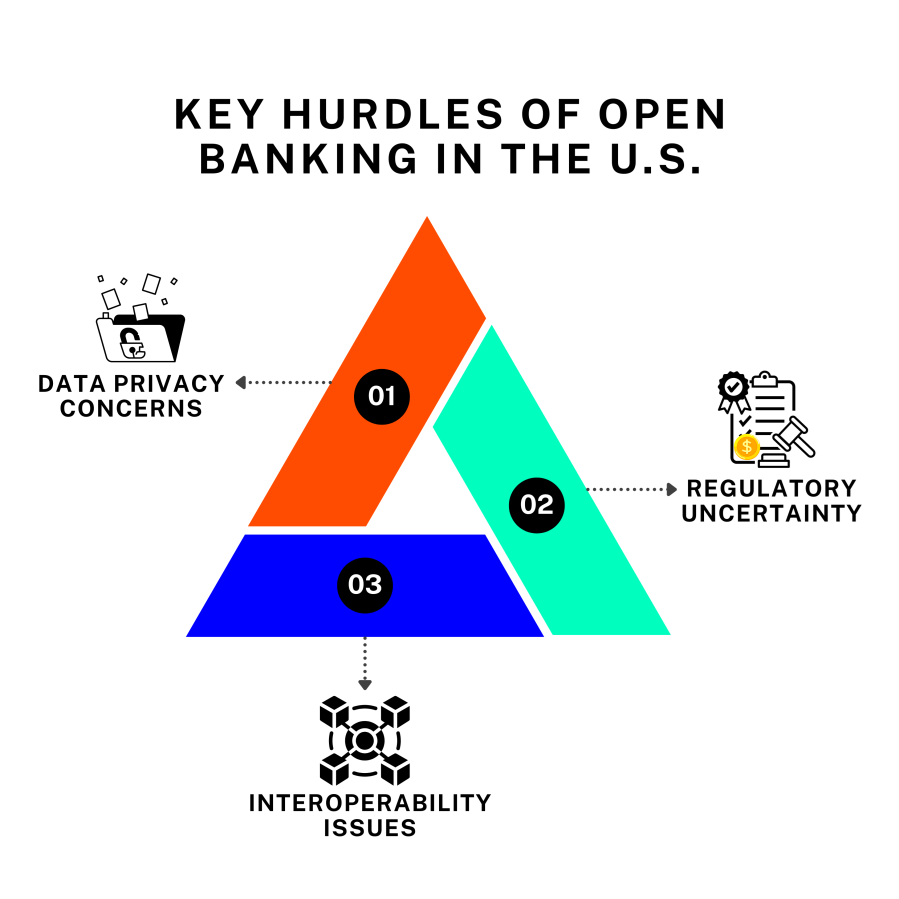

Key hurdles of Open Banking include:

- Data Privacy Concerns: Customers may not want to disclose this information when all remedies are not guaranteed protection.

- Regulatory Uncertainty: There is confusion in the compliance process where no strict rules are given.

- Interoperability Issues: Resolve on standardization of the exchange of data is crucial when banks and fintechs work together.

Open Banking has received much attention in the U.S. due to the customer’s rights for enhanced control over the financial information and opportunities to receive rather relevant services. The open-banking is not legally enacted in the US as it is in the EU, but, the market is already introducing APIs and setting up norms on its own.

Open Banking in its development process in the United States can contribute to the financial inclusion, stimulate innovation and intensification of competition between financial institutions and start-ups in the financial sector. Finally, as the U.S will continue to move forward in the next steps towards Open Banking, the future for financial services is as bright as can be.